The Bearing Steel Market is to Operate in Weakness Consolidation State in August

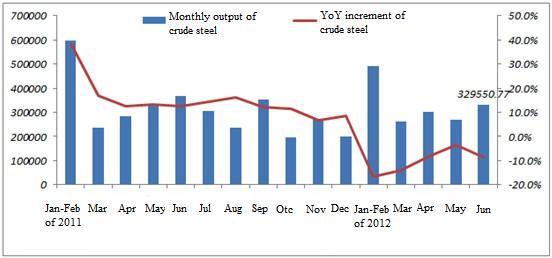

Figure 1: Change in Domestic Output of Bearing Steel (crude steel) from 2011 to 2012

Data Resource: Special Steel Association

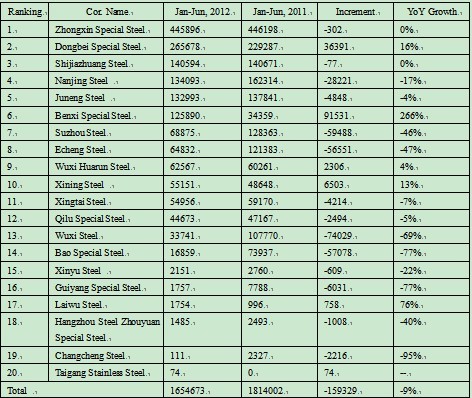

Table 1: Domestic Output of Crude Steel by Bearing Steel Manufacturers from January to June in 2012 (Unit: ton)

Figure 1: Change in Domestic Output of Bearing Steel (crude steel) from 2011 to 2012

Data Resource: Special Steel Association

Table 1: Domestic Output of Crude Steel by Bearing Steel Manufacturers from January to June in 2012 (Unit: ton)

Seen from Table 1 that the top three for bearing steel output from January to June in 2012 are Zhongxin Special Steel (Xinye Steel and Xingcheng Special Steel), Dongbei Speical Steel and Nanjing Steel, and the rankings of other steel mills bore only small change (for Sha Steel, only the yield of Huai Steel counted). Taigang Stainless Steel was on the list for the first time.

II. Performance of Domestic Bearing Steel Market in July:

The bearing steel price fell sharply in July, traders did poorly in transactions, shipments remained weak, and downstream enterprises showed negative procurement attitude. The mentality of market participants got worse due to the fast drop in price. Although the price of building materials slighly rose, it failed to warm the whole bearing steel market. The detailed situations of bearing steel market across the country in July are as follows:

The bearing steel price in Hangzhou market dropped sharply, and the deal was extermely light. Up to the end of July, the average knock-down price of standard GCr15 continuous casting non-annealed steel was from 4,730 to 4,850 yuan/ton, and the average knock-down price of GCr15 die-casting annealed steel was between 7,500 and 7,600 yuan/ton.

The bearing steel price in Luoyang market declined and the deal was light. Up to the end of July, the average knock-down price of standard GCr15 continuous casting non-annealed steel was from 4,950 to 5,100 yuan/ton, and the average knock-down price of GCr15 die-casting annealed steel was around 7,600 yuan/ton.

The bearing steel price in Xi'an market slightly dropped and the deal was light. Up to the end of July, the spot goods of standard GCr15 continuous casting non-annealed steel was relatively insufficient, and the average knock-down price of GCr15 die-casting annealed steel was around 7,500 yuan/ton.

As for Chongqing and Chengdu markets, the price went down in the weak trend, and the deal was common. Up to the end of July, the average knock-down price of standard GCr15 continuous casting non-annealed steel was from 5800 to 5900 yuan/ton, and the average knock-down price of GCr15 die-casting annealed steel was between 7,500 and 7,600 yuan/ton.

Seen from Table 1 that the top three for bearing steel output from January to June in 2012 are Zhongxin Special Steel (Xinye Steel and Xingcheng Special Steel), Dongbei Speical Steel and Nanjing Steel, and the rankings of other steel mills bore only small change (for Sha Steel, only the yield of Huai Steel counted). Taigang Stainless Steel was on the list for the first time.

II. Performance of Domestic Bearing Steel Market in July:

The bearing steel price fell sharply in July, traders did poorly in transactions, shipments remained weak, and downstream enterprises showed negative procurement attitude. The mentality of market participants got worse due to the fast drop in price. Although the price of building materials slighly rose, it failed to warm the whole bearing steel market. The detailed situations of bearing steel market across the country in July are as follows:

The bearing steel price in Hangzhou market dropped sharply, and the deal was extermely light. Up to the end of July, the average knock-down price of standard GCr15 continuous casting non-annealed steel was from 4,730 to 4,850 yuan/ton, and the average knock-down price of GCr15 die-casting annealed steel was between 7,500 and 7,600 yuan/ton.

The bearing steel price in Luoyang market declined and the deal was light. Up to the end of July, the average knock-down price of standard GCr15 continuous casting non-annealed steel was from 4,950 to 5,100 yuan/ton, and the average knock-down price of GCr15 die-casting annealed steel was around 7,600 yuan/ton.

The bearing steel price in Xi'an market slightly dropped and the deal was light. Up to the end of July, the spot goods of standard GCr15 continuous casting non-annealed steel was relatively insufficient, and the average knock-down price of GCr15 die-casting annealed steel was around 7,500 yuan/ton.

As for Chongqing and Chengdu markets, the price went down in the weak trend, and the deal was common. Up to the end of July, the average knock-down price of standard GCr15 continuous casting non-annealed steel was from 5800 to 5900 yuan/ton, and the average knock-down price of GCr15 die-casting annealed steel was between 7,500 and 7,600 yuan/ton.

Figure 2: Average Price Trend of Domestic Bearing Steel from 2011 to 2012

Data Resource: Mysteel

According to the statistics from Mysteeel.com: up to the end of July, 2012, the average price of GCr15 Φ50mm continuous casting non-annealed steel in China was 5,407 yuan/ton; the average price of GCr15 Φ100mm die-casting annealed steel was 8,021 yuan/ton. (some modifications applied to the statistical method)

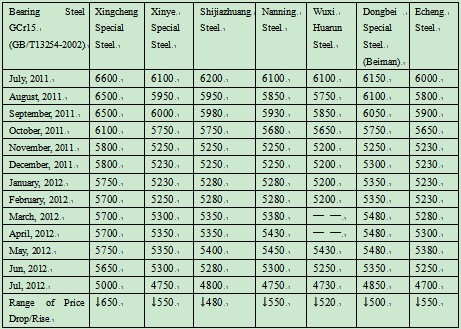

Table 2: Summary of Sales Price of Major Bearing Steel Manufacturers in East China (standard continuous casting non-annealed steel bar) Unit: yuan

Figure 2: Average Price Trend of Domestic Bearing Steel from 2011 to 2012

Data Resource: Mysteel

According to the statistics from Mysteeel.com: up to the end of July, 2012, the average price of GCr15 Φ50mm continuous casting non-annealed steel in China was 5,407 yuan/ton; the average price of GCr15 Φ100mm die-casting annealed steel was 8,021 yuan/ton. (some modifications applied to the statistical method)

Table 2: Summary of Sales Price of Major Bearing Steel Manufacturers in East China (standard continuous casting non-annealed steel bar) Unit: yuan

Table 2 shows that the bearing steel price in East China dropped sharply in July. Instead of rush shipment, manufacturers mainly held the wait and see attitude, which may resulted from the sluggish transactions and heavy losses these days.

III. Domestic Bearing Steel Market will Experience Vulnerable Consolidation:

1. Raw materials

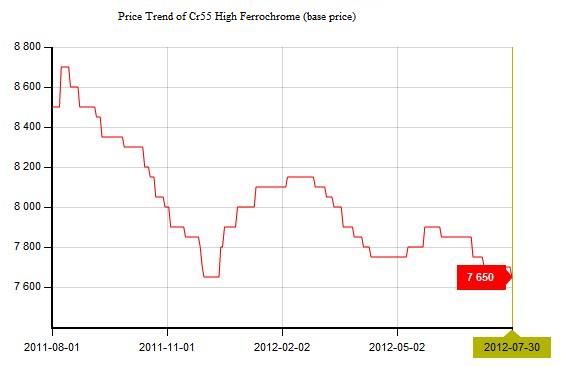

The high-chrome prices dropped in July, and the quoted price at the end of the month was around 7650 yuan/ton, 100 yuan/ton fell compared with last month. The price drop of coal chemical products further pushed the deterioration of the environment of bearing steel market.

Table 2 shows that the bearing steel price in East China dropped sharply in July. Instead of rush shipment, manufacturers mainly held the wait and see attitude, which may resulted from the sluggish transactions and heavy losses these days.

III. Domestic Bearing Steel Market will Experience Vulnerable Consolidation:

1. Raw materials

The high-chrome prices dropped in July, and the quoted price at the end of the month was around 7650 yuan/ton, 100 yuan/ton fell compared with last month. The price drop of coal chemical products further pushed the deterioration of the environment of bearing steel market.

Figure 3: Average Price Trend of Domestic High Carbon Ferrochrome from 2011 to 2012

Data Resource: Mysteel

2. Steel Mills

In mid July, the estimated daily outputs of crude steel, pig iron, steel and coke are respectively 1.9933, 1.8441, 2.8044 and 1.336 million tons, wherein, the estimated daily output of crude steel experienced an increase of 35.2 thousand tons compared to the beginning of the same month; the estimated accumulated crude steel output was up to 1.9823 million tons. From January to June, the total sales revenue of large and medium-sized steel enterprises was 1.79575 trillion yuan, down 3.34% year on year; profits of 39.258 billion yuan, down 59.8%; profit of 2.385 billion yuan, down 95.81 %. The industry loss widened to 33.75%, and the profit margin was 0.13%. The average daily sale of steel of 76 key steel enterprises in mid-July was 1.2104 million tons, down 37,800 tons compared with mid-June. The average sale price of steel of 76 key enterprises in mid-July was 4416 yuan/ton, down 73 yuan/ton compared to the beginning of July. It is learned that some steel mills have plans for overhaul of production lines and blast furnaces in August, but few are willing to substantially reduce the output of steel. The plant inventory level has increased, so steel mills are facing more pressure now.

3. Steel Market

The supply and demand pressures remains in the steel market, and the problem of excess production was now particularly serious due to the economic slowdown, causing great pressure to the market industry chain. On a short view, major steel mills will not cut back sharply, so the pressure of market supply and demand is difficult to be effectively released. For now, the impact of price cutting of future goods in August by steel mills has further spread in the market, the price decline in raw materials has greatly undermined the market confidence. When the market is in the price drop crisis, traders are accustomed to focus on the raw materials, hoping that the support of costs can help stabilizing the spot goods market, but on the present situation, the support benefit of costs has no longer existed. Recently, the macro trend is still negative, the policies fail to guide the market to the good direction, and the market is difficult to pick up in the short term.

4. Market Outlook

After the falling in July, the price inversion between market price and ex-factory price has further widened, which will drive the steel mills to reduce price again in early August, so the market is difficult to get warm in the short term due to the interaction.

At present, no significant change has occurred in the weakening trend of bearing steel market, the performance of emerging economies is not ideally good, and the price inversion of steel price will be the biggest pitfall of the aftermarket. We can feel that the market demand is getting improved very slowly, few hope can be seen from the appliance, automotive and other downstream industries. The market performance is far from optimistic, and the orders are rare.

In summary, the bearing steel market is to go down in the obvious downward trend, and is difficult to get improved soon.

Figure 3: Average Price Trend of Domestic High Carbon Ferrochrome from 2011 to 2012

Data Resource: Mysteel

2. Steel Mills

In mid July, the estimated daily outputs of crude steel, pig iron, steel and coke are respectively 1.9933, 1.8441, 2.8044 and 1.336 million tons, wherein, the estimated daily output of crude steel experienced an increase of 35.2 thousand tons compared to the beginning of the same month; the estimated accumulated crude steel output was up to 1.9823 million tons. From January to June, the total sales revenue of large and medium-sized steel enterprises was 1.79575 trillion yuan, down 3.34% year on year; profits of 39.258 billion yuan, down 59.8%; profit of 2.385 billion yuan, down 95.81 %. The industry loss widened to 33.75%, and the profit margin was 0.13%. The average daily sale of steel of 76 key steel enterprises in mid-July was 1.2104 million tons, down 37,800 tons compared with mid-June. The average sale price of steel of 76 key enterprises in mid-July was 4416 yuan/ton, down 73 yuan/ton compared to the beginning of July. It is learned that some steel mills have plans for overhaul of production lines and blast furnaces in August, but few are willing to substantially reduce the output of steel. The plant inventory level has increased, so steel mills are facing more pressure now.

3. Steel Market

The supply and demand pressures remains in the steel market, and the problem of excess production was now particularly serious due to the economic slowdown, causing great pressure to the market industry chain. On a short view, major steel mills will not cut back sharply, so the pressure of market supply and demand is difficult to be effectively released. For now, the impact of price cutting of future goods in August by steel mills has further spread in the market, the price decline in raw materials has greatly undermined the market confidence. When the market is in the price drop crisis, traders are accustomed to focus on the raw materials, hoping that the support of costs can help stabilizing the spot goods market, but on the present situation, the support benefit of costs has no longer existed. Recently, the macro trend is still negative, the policies fail to guide the market to the good direction, and the market is difficult to pick up in the short term.

4. Market Outlook

After the falling in July, the price inversion between market price and ex-factory price has further widened, which will drive the steel mills to reduce price again in early August, so the market is difficult to get warm in the short term due to the interaction.

At present, no significant change has occurred in the weakening trend of bearing steel market, the performance of emerging economies is not ideally good, and the price inversion of steel price will be the biggest pitfall of the aftermarket. We can feel that the market demand is getting improved very slowly, few hope can be seen from the appliance, automotive and other downstream industries. The market performance is far from optimistic, and the orders are rare.

In summary, the bearing steel market is to go down in the obvious downward trend, and is difficult to get improved soon.

1.The news above mentioned with detailed source are from internet.We are trying our best to assure they are accurate ,timely and safe so as to let bearing users and sellers read more related info.However, it doesn't mean we agree with any point of view referred in above contents and we are not responsible for the authenticity. If you want to publish the news,please note the source and you will be legally responsible for the news published.

2.All news edited and translated by us are specially noted the source"CBCC".

3.For investors,please be cautious for all news.We don't bear any damage brought by late and inaccurate news.

4.If the news we published involves copyright of yours,just let us know.

Next Aug 17 Bearing Steel Price in Different Regions of China

BRIEF INTRODUCTION

Cnbearing is the No.1 bearing inquiry system and information service in China, dedicated to helping all bearing users and sellers throughout the world.

Cnbearing is supported by China National Bearing Industry Association, whose operation online is charged by China Bearing Unisun Tech. Co., Ltd.

China Bearing Unisun Tech. Co., Ltd owns all the rights. Since 2000, over 3,000 companies have been registered and enjoyed the company' s complete skillful service, which ranking many aspects in bearing industry at home and abroad with the most authority practical devices in China.