Bearing steel price will fluctuate downwards in June

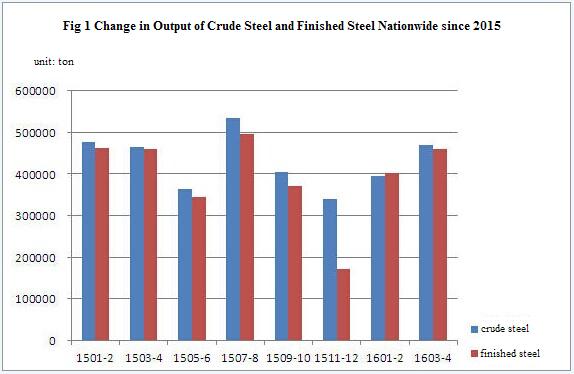

2. Output of finished bearing steel from January to April: decreased YoY as reported by the majority of steel mills

2. Output of finished bearing steel from January to April: decreased YoY as reported by the majority of steel mills

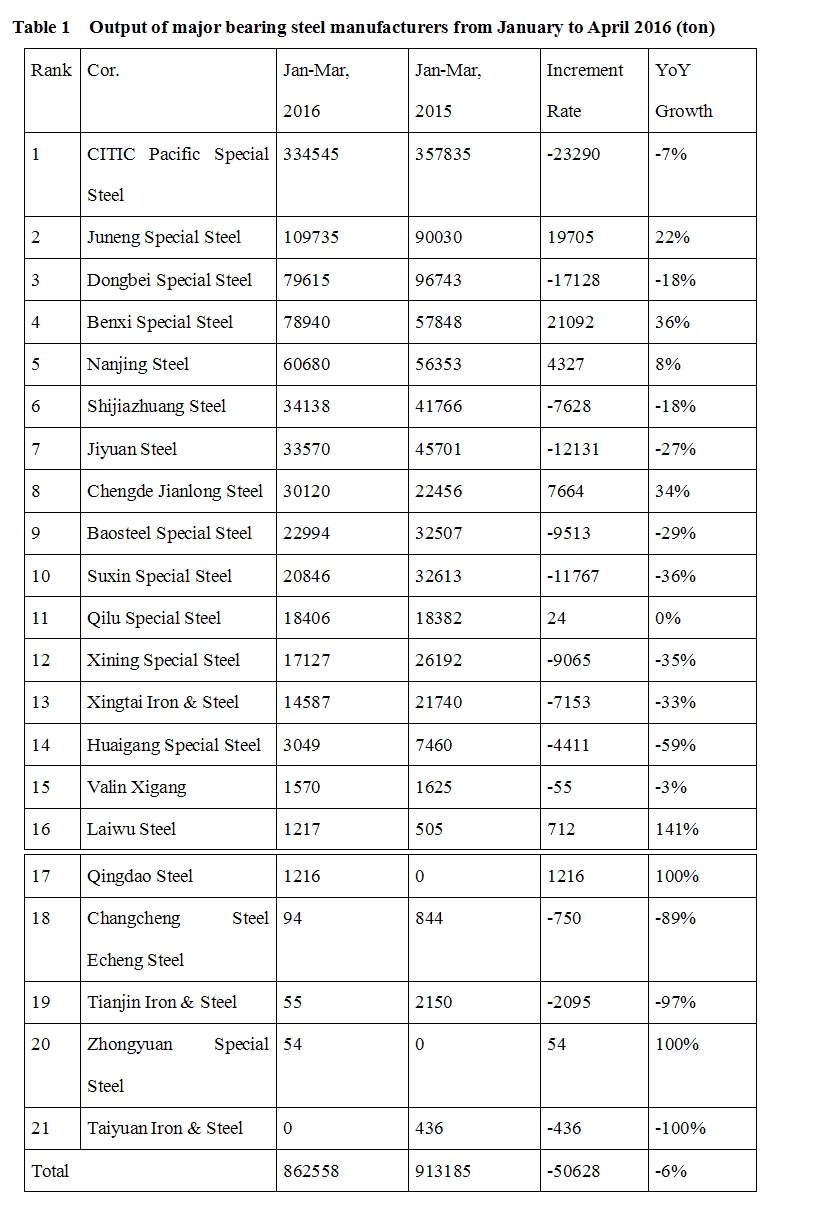

Seen from Table 1 that the top three for bearing steel output from January to March 2016 are still Zhongxin Special Steel (Xinye Steel and Xingcheng Special Steel), Juneng Steel and Dongbei Speical Steel. (for Sha Steel, only the yield of Huai Steel is counted). Among these 21 companies, 8 reported increase in the crude bearing steel ouput, 12 companies reduced output and 1 was out of production. Although the total output has fallen compared with last year, the production capability in bearing steel market constantly releases. This is especially obvious in the second tier steel mills, the resource competition among which will be heating up, while the first tier steel mills remains stable in production.

II. Bearing Steel Markets

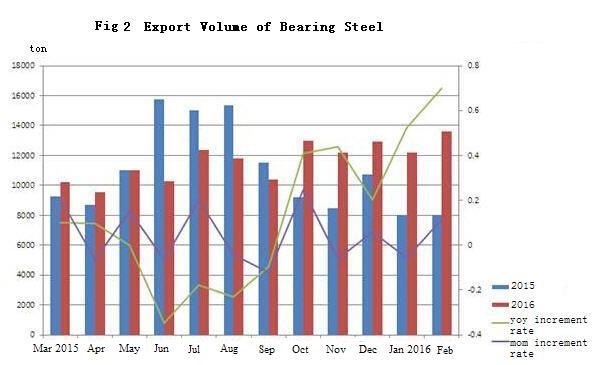

1. Bearing steel exports increased YoY in April

According to the statistics from domestic 8 major bearing steel production enterprises: Domestic bearing steel export was 13,518 tons in April, 103 tons more compared with the previous month, increased by 41.62% YoY and 0.77% MoM. Seen from Figure 2 that the top three on the list of bearing steel export volume are still Xingcheng Special Steel, Daye Speical Steel and Dongbei Speical Steel. Wherein, Xingcheng Special Steel reported the largest export volume of bearing steel, 12,275 tons, accounting for the vast majority of bearing steel exports.

Seen from Table 1 that the top three for bearing steel output from January to March 2016 are still Zhongxin Special Steel (Xinye Steel and Xingcheng Special Steel), Juneng Steel and Dongbei Speical Steel. (for Sha Steel, only the yield of Huai Steel is counted). Among these 21 companies, 8 reported increase in the crude bearing steel ouput, 12 companies reduced output and 1 was out of production. Although the total output has fallen compared with last year, the production capability in bearing steel market constantly releases. This is especially obvious in the second tier steel mills, the resource competition among which will be heating up, while the first tier steel mills remains stable in production.

II. Bearing Steel Markets

1. Bearing steel exports increased YoY in April

According to the statistics from domestic 8 major bearing steel production enterprises: Domestic bearing steel export was 13,518 tons in April, 103 tons more compared with the previous month, increased by 41.62% YoY and 0.77% MoM. Seen from Figure 2 that the top three on the list of bearing steel export volume are still Xingcheng Special Steel, Daye Speical Steel and Dongbei Speical Steel. Wherein, Xingcheng Special Steel reported the largest export volume of bearing steel, 12,275 tons, accounting for the vast majority of bearing steel exports.

2. Bearing steel prices were mixed in May

Bearing steel prices were mixed in May. This month, the prices of common continuous casting and rolling bearing steels reported by the first tier steel mills were relatively strong, individual steel mills slightly raised the prices; the second and third tier bearing steel mills were in intense competition because of poor sales. Except Beiman Special Steel and Xingcheng Special Steel which reported slight increase in prices, Jiyuan Steel, Xingtai Iron & Steel, Juneng Steel, Chengde Jianlong Steel and other steel mills all fell in price, mainly in the range of 200-300 yuan/ton.

The main reason is that the current market performance is poor, wherein, the overall yield reported by steel mills is high and traders have less shipments. As for the market outlook in June, the balance of supply and demand is to be broken with the increase in steel production, and bearing steel prices are more likely to fall for most of the steel mills.

2. Bearing steel prices were mixed in May

Bearing steel prices were mixed in May. This month, the prices of common continuous casting and rolling bearing steels reported by the first tier steel mills were relatively strong, individual steel mills slightly raised the prices; the second and third tier bearing steel mills were in intense competition because of poor sales. Except Beiman Special Steel and Xingcheng Special Steel which reported slight increase in prices, Jiyuan Steel, Xingtai Iron & Steel, Juneng Steel, Chengde Jianlong Steel and other steel mills all fell in price, mainly in the range of 200-300 yuan/ton.

The main reason is that the current market performance is poor, wherein, the overall yield reported by steel mills is high and traders have less shipments. As for the market outlook in June, the balance of supply and demand is to be broken with the increase in steel production, and bearing steel prices are more likely to fall for most of the steel mills.

III. Relevant Markets

1. Raw materials market

III. Relevant Markets

1. Raw materials market

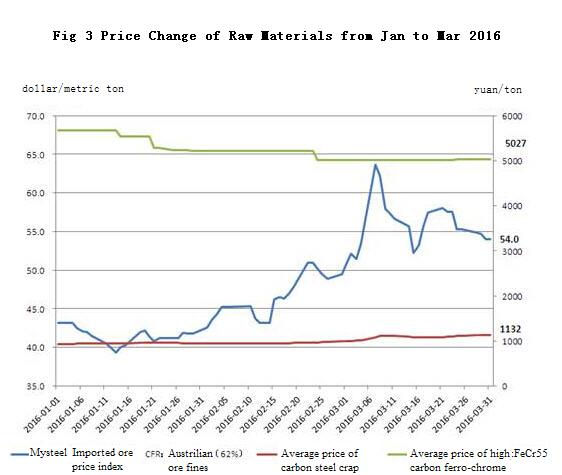

Imported ore price ran in consolidation in May, closed at 51.5 dollar/ton by the end of the month; the price of carbon steel scrap was in the weak trend, closed at 1220 yuan/ton by the end of the month, up by 17.57% over the previous month; the price of high carbon ferrochrome was slightly adjusted natiowide, closed at 6003 yuan/ton by the end of the month. Combined with the current supply and demand situation, the supply pressure remains, and the raw materials market is expected to run in weak consolidation in June when the price of finished products goes down.

2. Downstream market

According to the statistical analysis of China Association of Automobile Manufacturers, the output and sales of automobiles decreased YoY and MoM in April, but the overall performance was relatively good.

The output and sales of automobiles were respectively 2.17 million and 2.122 million units in April, decreased by 13.9% and 13% MoM and increased by 4.3% and 6.3% YoY. From January to April, the output and sales of automobiles were 8.76 million and 8.65 million units, increased by 5.7% and 6.1% YoY. Wherein, the output and sales of passenger cars were 7.537 million and 7.448 million units, increased by 6.6% and 6.7% YoY; the output and sales of commercial vehicles were 1.223 million and 1.202 millionunits, increased by 0.6% and 2.7% YoY.

Imported ore price ran in consolidation in May, closed at 51.5 dollar/ton by the end of the month; the price of carbon steel scrap was in the weak trend, closed at 1220 yuan/ton by the end of the month, up by 17.57% over the previous month; the price of high carbon ferrochrome was slightly adjusted natiowide, closed at 6003 yuan/ton by the end of the month. Combined with the current supply and demand situation, the supply pressure remains, and the raw materials market is expected to run in weak consolidation in June when the price of finished products goes down.

2. Downstream market

According to the statistical analysis of China Association of Automobile Manufacturers, the output and sales of automobiles decreased YoY and MoM in April, but the overall performance was relatively good.

The output and sales of automobiles were respectively 2.17 million and 2.122 million units in April, decreased by 13.9% and 13% MoM and increased by 4.3% and 6.3% YoY. From January to April, the output and sales of automobiles were 8.76 million and 8.65 million units, increased by 5.7% and 6.1% YoY. Wherein, the output and sales of passenger cars were 7.537 million and 7.448 million units, increased by 6.6% and 6.7% YoY; the output and sales of commercial vehicles were 1.223 million and 1.202 millionunits, increased by 0.6% and 2.7% YoY.

IV. Conclusion

Recalling the bearing steel market in May, the pressure on the balance between supply and demand is gradually increasing, and the upward momentum has halted. Xingcheng Special Steel and BaoSteel Special-Steel take lead in the high-end market for their excellent quality, and the prices are not affected by the market, still much higher than other steel mills. Benxi Iron and Steel, Juneng Steel, Jianlong Steel and other steel mills gradually operate at full capacity, and resources in bearing steel market are increasingly abundant, gradually revealing a situation of oversupply. The price competition in the second-tier materials market is relatively intense.

Major steel mills rarely cut output for maintenance as the contradiction of supply exceeding demand is still sharp in June, and there will not be a substantial rebound on downstream business demand in the short term. If production release can not be well controlled, the price competition in bearing market will be more competitive and the weak trend will continue.

In summary, the price in bearing steel market is expected to go down in shocks in June, but the price may be slightly pushed up if some first-tier steel mills were in resource shortage.

IV. Conclusion

Recalling the bearing steel market in May, the pressure on the balance between supply and demand is gradually increasing, and the upward momentum has halted. Xingcheng Special Steel and BaoSteel Special-Steel take lead in the high-end market for their excellent quality, and the prices are not affected by the market, still much higher than other steel mills. Benxi Iron and Steel, Juneng Steel, Jianlong Steel and other steel mills gradually operate at full capacity, and resources in bearing steel market are increasingly abundant, gradually revealing a situation of oversupply. The price competition in the second-tier materials market is relatively intense.

Major steel mills rarely cut output for maintenance as the contradiction of supply exceeding demand is still sharp in June, and there will not be a substantial rebound on downstream business demand in the short term. If production release can not be well controlled, the price competition in bearing market will be more competitive and the weak trend will continue.

In summary, the price in bearing steel market is expected to go down in shocks in June, but the price may be slightly pushed up if some first-tier steel mills were in resource shortage.

1.The news above mentioned with detailed source are from internet.We are trying our best to assure they are accurate ,timely and safe so as to let bearing users and sellers read more related info.However, it doesn't mean we agree with any point of view referred in above contents and we are not responsible for the authenticity. If you want to publish the news,please note the source and you will be legally responsible for the news published.

2.All news edited and translated by us are specially noted the source"CBCC".

3.For investors,please be cautious for all news.We don't bear any damage brought by late and inaccurate news.

4.If the news we published involves copyright of yours,just let us know.

Next Aug 17 Bearing Steel Price in Different Regions of China

BRIEF INTRODUCTION

Cnbearing is the No.1 bearing inquiry system and information service in China, dedicated to helping all bearing users and sellers throughout the world.

Cnbearing is supported by China National Bearing Industry Association, whose operation online is charged by China Bearing Unisun Tech. Co., Ltd.

China Bearing Unisun Tech. Co., Ltd owns all the rights. Since 2000, over 3,000 companies have been registered and enjoyed the company' s complete skillful service, which ranking many aspects in bearing industry at home and abroad with the most authority practical devices in China.